Investors have been reallocating capital out of Amazon ($AMZN) shares fairly heavily since the company reported a lackluster fourth quarter earnings report. After peaking over $400 in January the stock has dropped about 75 points to the low 300's. In fact, I actually think the stock is beginning to look compelling for long term investors, if you believe Amazon will continue to successfully enter new markets, as the shares now fetch only about 1.5 times 2014 revenue (after deducting net cash). While profit margins remain low (cash flow of $5.5 billion in 2013 equated to only 7.4% of sales), those that claim Amazon makes no money don't seem to dig into the company's financial statements very deeply.

All of that said, after looking at Amazon's sales trends over the last 15 years, I believe that Wall Street is currently overly optimistic about sales growth at Amazon for the next two years. If you believe that investors will be focused on sales growth, in lieu of material profit margin gains in the intermediate term, it would imply that Amazon bulls can take their time building long-term investments in the stock over coming quarters.

So why do I think Amazon will be hard-pressed to achieve the current consensus estimates for sales in 2014 (up 21% to $89.9 billion) and 2015 (up another 20% to $107.6 billion). First, let's look at Amazon's annual sales since 1998:

Simply looking at this data may cause you to feel pretty upbeat about Amazon's business. Over the past 15 years sales have grown an astounding 41% per year, rising from under $1 billion in 1998 to nearly $75 billion in 2013. Is it really a stretch to asssume that two more years of 20%+ growth could be in the cards?

The problem Amazon is going to begin to face is the fact that once you reach a certain size, it becomes nearly impossible to continue to grow at 40%, 30%, or even 20% per year. Finding an additional $15.4 billion of revenue in a single year (the incremental figure analysts estimate Amazon will book in 2014) is no easy feat. In fact, Amazon's total revenue in 2007 was just $14.8 billion, so "2014 Amazon" must equal "2013 Amazon" plus "2007 Amazon." With annual revenue approaching the $100 billion level, the company's growth rate is likely to begin to slow soon.

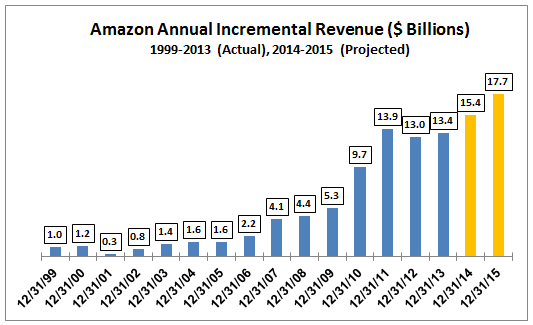

Is there any way to know when exactly growth will decline significantly? Not really, but one of the numbers I like to focus on is incremental revenue growth, in dollars, from one year to the next. As a company gets larger and larger, the amount of incremental sales growth needed simply to maintain its growth rate rises fairly sharply. In fact, if we chart out Amazon's incremental annual sales growth since 1999, we can see patterns emerge:

For instance, between 1999 and 2006 Amazon was able to grow sales by between $1-2 billion a year (roughly). That figure rose to $4-5 billion from 2007-2009, and accelerated to $10 billion in 2010 after the recession ended. Interestingly, over the last three years Amazon has hit a wall. In both 2012 and 2013, incremental sales growth at Amazon failed to eclipse 2011 levels. I believe this could be the beginning of a period where we see Amazon's sales growth slow materially.

Perhaps problematic, the current Wall Street consensus forecast calls for Amazon's incremental revenue growth in dollars to reaccelerate to more than $15 billion this year, and again to nearly $18 billion in 2015 (look at the orange bars in the above chart). While there is no assurance that this figure cannot continue to climb, there will be a time when Amazon simply cannot continue to find that much new revenue each and every year (without making large acquisitions anyway, not something they have typically done). Given that a disappointment in merchandise sales growth has been a key driver of Amazon's recent stock market weakness, I believe it is entirely possible that both 2014 and 2015 sales forecasts are too high. Maintaining annual sales growth of 20% for much longer seems unlikely, perhaps even starting this year.

As I mentioned at the outset of this article, however, I don't necessarily think this would spell the end of Amazon's stock market stardom, at least not long term. If Jeff Bezos is willing to show investors that he is willing to demonstrate that profit margins can be susteained at levels above those currently being attained, investors would likely be very pleased and any short term stock decline would quickly be reversed. After all, annual sales approaching $100 billion offer Amazon the ability to generate some very impressive free cash flow, which would make the stock's current market value of $150 billion seem not so unreasonable.

In coming quarters, I will be focused on Amazon's sales trends and if I am correct and the current consensus forecasts are too aggressive, any continued short-term weakness in Amazon shares could present investors with an excellent opportunity to continue building a long-term position in the stock.

Full Disclosure: Long AMZN at the time of writing, but positions may change at any time